/Project Details

Bitcoin Attention with Google Trends Data

A time-series econometrics pipeline examining how Google Trends-style public attention relates to Bitcoin volatility, volume, and returns.

This project studies Bitcoin as an attention-driven market. The central question is whether Google Trends-style search attention helps explain Bitcoin volatility, trading volume, and returns, or whether market movements predict public attention.

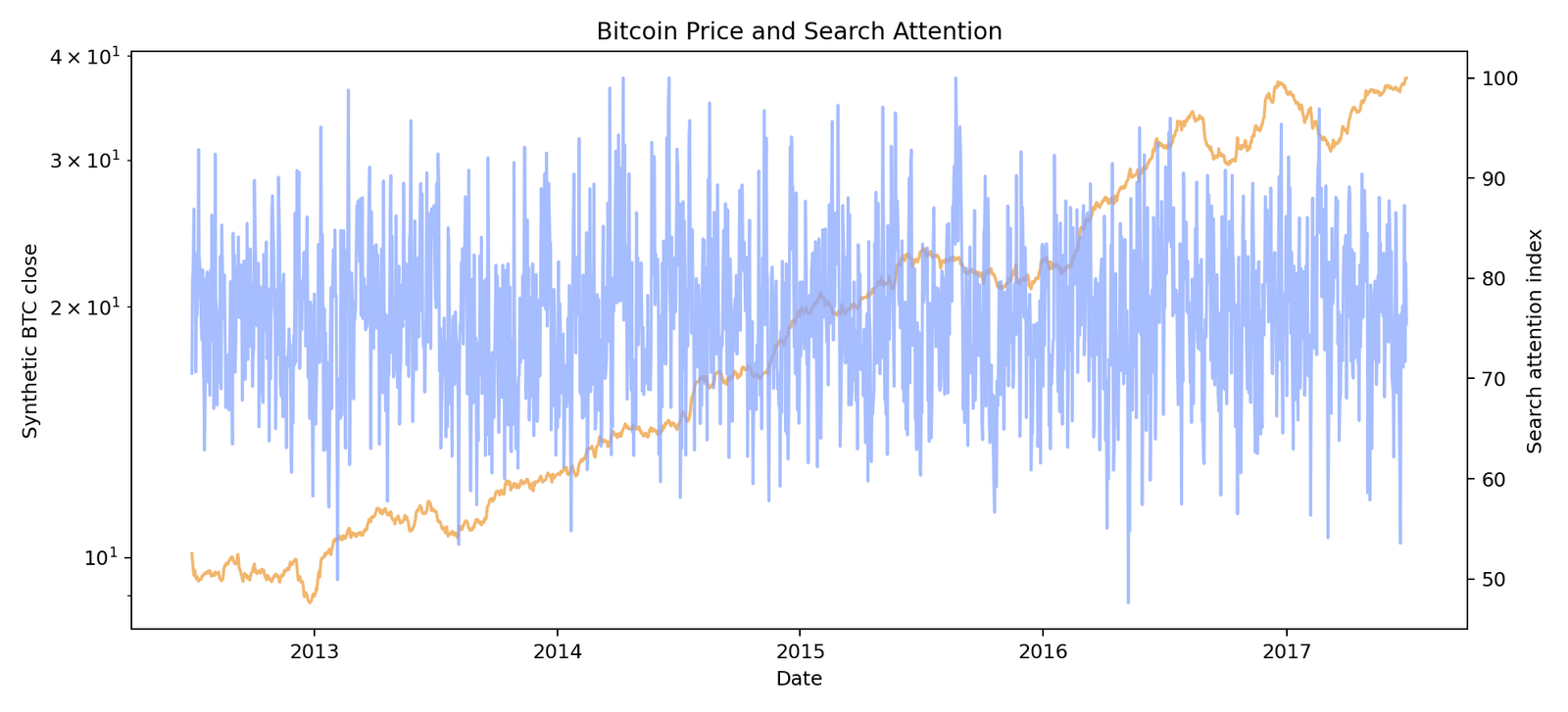

The workflow processes Bitcoin OHLCV files and Google Trends exports, constructs variables such as log returns, realized volatility, log volume, standardized search intensity, and log search quantity, and then estimates Vector Autoregression models.

Rather than treating attention as a vague narrative, the project frames it as a measurable time-series signal that can be tested against market dynamics with formal econometric tools.

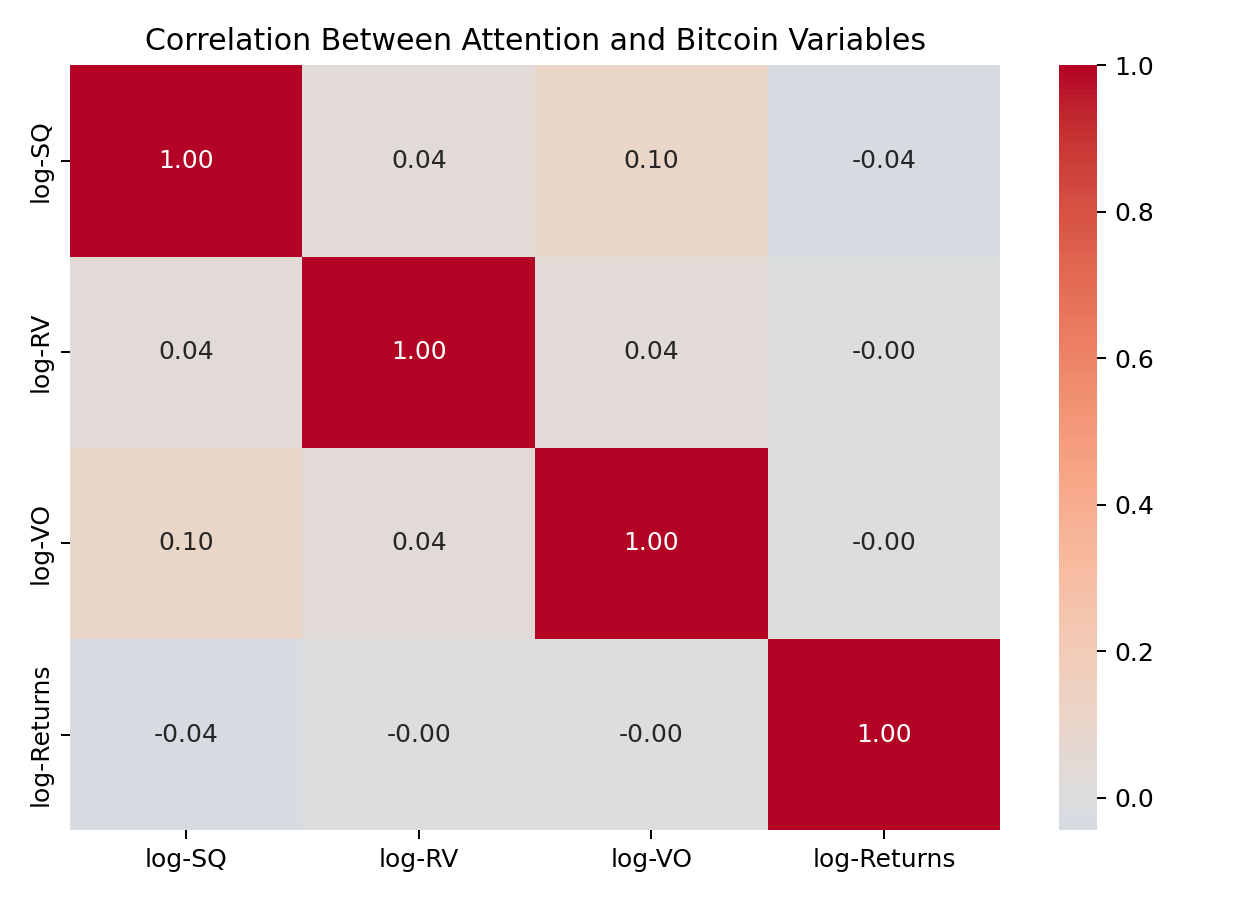

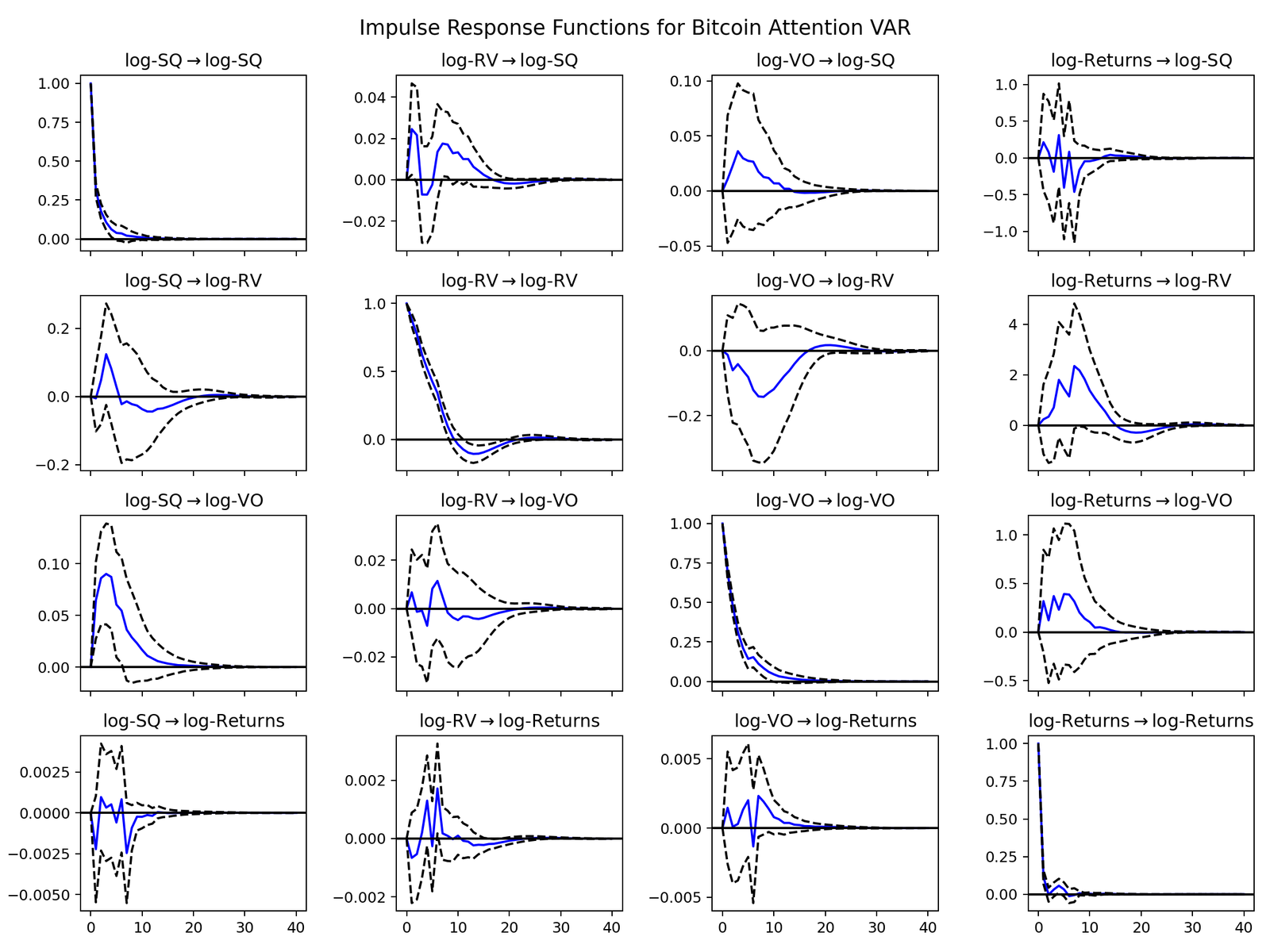

The analysis includes descriptive statistics, multiple VAR specifications, Granger causality tests, impulse response functions, and a subsample view around a structural-break-style date.

From a portfolio perspective, the project highlights a different side of my work: time-series preprocessing, behavioral finance reasoning, statistical modeling, and interpretation of dynamic systems.

Highlights

- Processed Bitcoin-style OHLCV and Google Trends-style attention data into synchronized daily time series.

- Engineered log returns, realized volatility, log volume, standardized search intensity, and log search quantity variables.

- Estimated VAR systems linking attention, volatility, volume, and returns.

- Ran Granger causality tests to inspect predictive direction between public attention and market variables.

- Generated impulse response functions to visualize dynamic shock propagation.

- Included a structural-break-style subsample perspective to compare behavior across different market regimes.

Figures